Public Finance Data and Analysis

Free and Open Access to

The Sri Lankan Central Bank’s issue of a 30 year Bond on February 27, 2015 ran into immediate controversy. The main reason was that markets were expecting the Bank to take up only around one billion rupees, but the Bank accepted bids upwards of ten billion rupees. The weighted average rate of return paid on the bond was also driven up by the excess uptake (the term ‘interest rate’ will be used for this, instead of ‘yield’, for reader simplicity).

The public outcry that has followed this unexpected move by the Central Bank comprised two concerns. One is the high uptake at a high interest rate. The second is that the largest beneficiary of the issue was a company that is closely connected to the sitting governor of the Central Bank – creating a serious conflict of interest for the Governor’s involvement in any decisions on the bids. The political and bureaucratic establishments of Sri Lanka have very poor rules and controls with regard to managing conflicts of interest, which have over time become rampant. Public focus on this problem is hence a positive development.

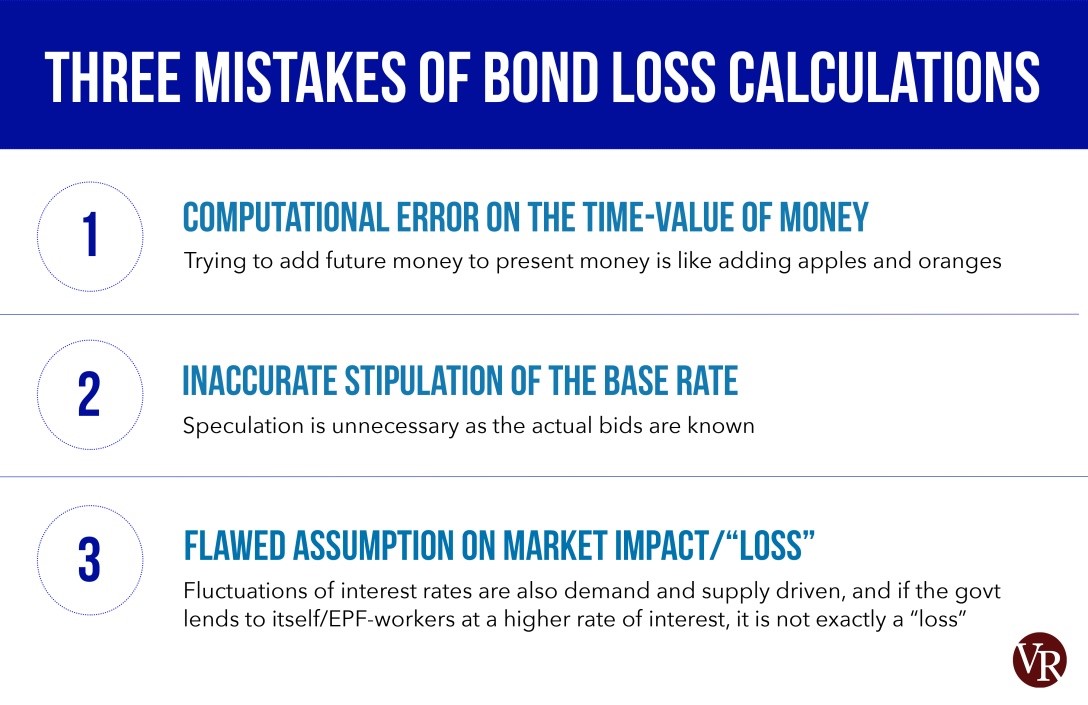

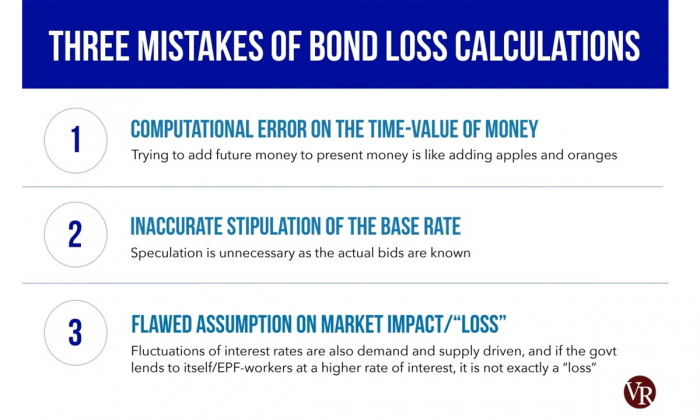

The first aspect of the problem- of a high uptake at a high interest rate- has led to a series of articles in newspapers that have attempted to calculate the ‘loss’ that has resulted from the high rate. That the question has been asked, and many contributions made, including by the ex-Governor of the Central Bank, is again a positive development. Unfortunately, the contributions published to-date suffer from a combination of three problems; (1) a computational error on the time-value of money, (2) an inaccurate stipulation of the counterfactual-rate, and (3) a flawed assumption with regard to market impact and ‘loss’.

Computational Error on the Time-Value of Money

This error was first highlighted by an article published in the Sri Lankan FT by Dr. Udara Peiris, now a tenured professor of finance at the National Research University Higher School of Economics, Moscow, Russia (for that article see http://www.ft.lk/2015/04/29/a-clarification-on-the-cost-of-the-bond-scandal/).

The error made is the failure to recognise that trying to add future money to present money is like adding apples and oranges. All money that is added up to calculate loss must first be computed to its value at a specific time, and the loss should be stated in terms of the loss at that time. If a person lost Rs. 1,000 today, and interest rates are 10.4%, it is the same as losing Rs. 2,000 seven years later, or Rs. 4,000 fourteen years later (money doubles every 7 years when kept at a compounded annual interest rate of 10.4%). Therefore losing Rs. 1,000 today and losing a further Rs. 4,000 fourteen years later is not the same as losing Rs. 5,000 today. It is only the same as losing Rs. 2,000 today.

The time-value of money is a basic and core principle of financial calculations and the press articles, apart from Dr. Peiris’, seem to have ignored it. The result has been erroneous calculations that add up money due in 20 and 30 years with money due in the present year, without discounting future payments to the present value. The result is incorrect calculations that hugely exaggerate the loss.

Inaccurate Stipulation of the Counterfactual-Rate

All calculations of loss are based on estimating the ‘extra’ interest that was paid for the 30 year bond, above and beyond some counterfactual-rate – that is, the rate that would have been paid had the bond issue not been controversially increased by a multiple of 10 times.

Various rates are used by writers, all of them well under 10% - some based on signals given by the Central Bank before the issue, others based on similar bond issues in the past, and yet others based on trading and yields in the secondary market. However, such speculation is not necessary, as the actual bids are known.

A Public Debt Department (PDD) document, leaked to the public domain through the internet (in a positive act of whistle-blowing), provides details of all the bids accepted, and this has over time received significant circulation. The document shows that the market was not offering the Central Bank the low rates of between 9.3% and 9.7% that it had signalled to the market in trying to set expectations, It was quoting significantly higher: if bids were not prorated, clearing the Rs. 1 billion mark would have meant accepting Rs. 1.308 billion (including a full Rs. 0.5 billion from the EPF). The average weighted return paid out then on the bids received would have been 10.465%.

The leaks to the press from the draft COPE report say that the PDD recommended taking bids up to Rs. 2.608 billion. The recommendation is not alarming as Rs. 2.358 billion of this total came from government controlled entities – Rs. 1.5 billion from the EPF and the rest from government banks, and none (even by proxy) from Perpetual Treasuries, which has been identified as the dubious bidder where the Governor has a conflict of interest. Even though the PDD recommended more than double the uptake of what was announced, which is not a good practice, such deviation – taking multiples of 2 to 3 times – had also been a regular practice in the past years (mostly on shorter tenure bonds), and did not risk unsettling the markets.

The weighted rate for the Rs. 2.608 billion uptake was 10.724% (PDD calculations). This then provides the actual counterfactual rate that needs no guess work – it is based on the actual bids received and the PDD recommended uptake. Calculations hitherto published have not taken account of this information and therefore have not used an appropriate –counterfactual rate in evaluating the loss.

The “loss”: in deviating from initial PDD recommendation

The final uptake of Rs. 10.058 billion came at a rate of 11.727%. The loss calculation therefore would be the difference between this rate and the counterfactual rate for the alternative decision of accepting bids of only Rs. 2.608 billion. The excess interest paid in increasing the uptake was therefore 1% (or 1.003% to be precise).

The present value of the loss for over 30 years, in taking Rs. 10.058 billion at this higher rate, rather than the lower counterfactual-rate, is equal to almost Rs. 0.9 billion (896,430,491 to be precise). This is a large loss. However, it is also only a fraction of the Rs. 8.7 billion loss erroneously calculated on this 30 year bond by, for instance, by the ex-Governor of the Central Bank. Of the Rs. 7.8 billion difference, Rs. 5.7 billion comes from the computational error, and Rs. 2.1 billion from speculating a different base-rate.

Flawed assumption on market impact/”loss”

The lion share of the losses calculated by various contributors are not on the 30 year bond itself, but on subsequent bonds sold in the market, attributing their higher interest rates, as against the past, as a spill-over impact and the difference in interest cost (erroneously calculated without time-value adjustment) as the ‘loss’. It is assumed that the difference in the rate on subsequent bond sales from past rates on similar bonds is fully attributable to the markets being surprised on the 30 year bond. This is a flawed assumption for three reasons: (a) Fluctuations of government interest rates cannot be interpreted simplistically as profit and loss to the government, when the interest rates are managed by the government for various purposes – to influence savings and consumption, to handle liquidity issues, and to manage exchange rates. (b) Interest rates are a price for borrowing driven by supply and demand – increasing borrowing demand increases prices (interest rates), and such changes in pricing have various balancing consequences. For instance, shifting from international borrowing towards local borrowing (as has happened in the first half of 2015) increases the government’s demand for local debt and will tend to increase interest rates, while protecting against future external debt pressures. (c) Local economic factors, private sector borrowing picking up, and reduced excess liquidity in the banking sector (another feature of 2015) also put upward pressure on interest rates.

Overall, the 10 times increase in the uptake of the 30 year bond did surprise the markets and increased the rate of the 30 year bond by 1%. Interest expectation could have been set lower. A surprise spike in the rate for the longer term bonds can result in spill-over effects on further government borrowing in the immediate after-math in the short term as well. But the effect of the surprise on short term rates is likely to be small and short-lived. The market bids themselves for the 30 year bond, without the 10 times multiple, already signalled that rates were pushing upwards). In any case, the forced impact on interest rates is small, as the government can always reject bids if it does not fit with its own expectations of where the rates should be, and because the government has huge captive funds through the EPF and its Banks, which are in any case the major borrowers at the higher rates. Furthermore, if the government is lending to itself (or to the EPF funds of workers) at a higher rate of interest, it is not accurate to describe this as a “loss”.

The biggest loss is Trust

If the government needed more funds, expanding borrowing on a rarely auctioned 30 year bond, that has the added function of price-discovery, was not the appropriate route.

Building stability and confidence are primary responsibilities of Central Banking. Spooking the markets and creating uncertainty by spiking the uptake on the 30 year bond auction cannot be credited as a responsible action.

While calculations of the resulting monetary loss have been erroneous and hugely exaggerated, the biggest loss is probably not monetary, it is the loss of trust and confidence. Sri Lanka’s Central Bank has seen an erosion of trust for some time and the advent of a new government and Governor created an opportunity to repair and restore trust. But the 30 year bond debacle, coupled with the weakness of investigations and accountability, has set back the Central Bank.