Topics

Explore

Featured Insight

Interest Costs Have Been Eating Up Revenue

In 2023, for the first time in history, the government spent 9% of its GDP on interest payments, which took up 80% of the government revenue. A high interest-to-revenue ratio can be severely detrimental to a country's debt sustainability. This high ratio creates a need to borrow more, undermining debt sustainability and leaving limited revenue for essential government spending and investments. The interest-to-revenue ratio has increased in recent years for two reasons. Revenue Fell Due to Tax Reductions in 2019 Government revenue as a share of GDP dropped from 12% in 2019 to 9% in 2020. This is mainly due to the newly elected government lowering several tax rates in 2019. Thus, the interest share of revenue increased to 71% in 2020 from 47% in 2019, even though the interest payments as a share of GDP remained at 6%. Interest Costs Surged Due to High Interest Rates and More Government Debt Interest expenditure as a share of GDP increased to 9% in 2023 from 6% in pre-2021. This is due to (1) the domestic interest rates skyrocketing to above 25% post-2021 from less than 10% in the prior years - mainly owing to tight monetary conditions and lack of access to foreign financing. (2) Central government debt also increased significantly from 81.9% in 2019 to 114.2% in 2022, leading to higher interest expenditure as the government had to pay more interest on the excessive debt obtained. It is also important to note that this interest figure would have been much higher if the accrued interest expenditure on defaulted foreign debt had been included.

Featured Insight

Interest Costs Have Been Eating Up Revenue

In 2023, for the first time in history, the government spent 9% of its GDP on interest payments, which took up 80% of the government revenue. A high interest-to-revenue ratio can be severely detrimental to a country's debt sustainability. This high ratio creates a need to borrow more, undermining debt sustainability and leaving limited revenue for essential government spending and investments. The interest-to-revenue ratio has increased in recent years for two reasons. Revenue Fell Due to Tax Reductions in 2019 Government revenue as a share of GDP dropped from 12% in 2019 to 9% in 2020. This is mainly due to the newly elected government lowering several tax rates in 2019. Thus, the interest share of revenue increased to 71% in 2020 from 47% in 2019, even though the interest payments as a share of GDP remained at 6%. Interest Costs Surged Due to High Interest Rates and More Government Debt Interest expenditure as a share of GDP increased to 9% in 2023 from 6% in pre-2021. This is due to (1) the domestic interest rates skyrocketing to above 25% post-2021 from less than 10% in the prior years - mainly owing to tight monetary conditions and lack of access to foreign financing. (2) Central government debt also increased significantly from 81.9% in 2019 to 114.2% in 2022, leading to higher interest expenditure as the government had to pay more interest on the excessive debt obtained. It is also important to note that this interest figure would have been much higher if the accrued interest expenditure on defaulted foreign debt had been included.

Featured Insight

Interest Costs Have Been Eating Up Revenue

In 2023, for the first time in history, the government spent 9% of its GDP on interest payments, which took up 80% of the government revenue. A high interest-to-revenue ratio can be severely detrimental to a country's debt sustainability. This high ratio creates a need to borrow more, undermining debt sustainability and leaving limited revenue for essential government spending and investments. The interest-to-revenue ratio has increased in recent years for two reasons. Revenue Fell Due to Tax Reductions in 2019 Government revenue as a share of GDP dropped from 12% in 2019 to 9% in 2020. This is mainly due to the newly elected government lowering several tax rates in 2019. Thus, the interest share of revenue increased to 71% in 2020 from 47% in 2019, even though the interest payments as a share of GDP remained at 6%. Interest Costs Surged Due to High Interest Rates and More Government Debt Interest expenditure as a share of GDP increased to 9% in 2023 from 6% in pre-2021. This is due to (1) the domestic interest rates skyrocketing to above 25% post-2021 from less than 10% in the prior years - mainly owing to tight monetary conditions and lack of access to foreign financing. (2) Central government debt also increased significantly from 81.9% in 2019 to 114.2% in 2022, leading to higher interest expenditure as the government had to pay more interest on the excessive debt obtained. It is also important to note that this interest figure would have been much higher if the accrued interest expenditure on defaulted foreign debt had been included.

Featured Insight

Interest Costs Have Been Eating Up Revenue

In 2023, for the first time in history, the government spent 9% of its GDP on interest payments, which took up 80% of the government revenue. A high interest-to-revenue ratio can be severely detrimental to a country's debt sustainability. This high ratio creates a need to borrow more, undermining debt sustainability and leaving limited revenue for essential government spending and investments. The interest-to-revenue ratio has increased in recent years for two reasons. Revenue Fell Due to Tax Reductions in 2019 Government revenue as a share of GDP dropped from 12% in 2019 to 9% in 2020. This is mainly due to the newly elected government lowering several tax rates in 2019. Thus, the interest share of revenue increased to 71% in 2020 from 47% in 2019, even though the interest payments as a share of GDP remained at 6%. Interest Costs Surged Due to High Interest Rates and More Government Debt Interest expenditure as a share of GDP increased to 9% in 2023 from 6% in pre-2021. This is due to (1) the domestic interest rates skyrocketing to above 25% post-2021 from less than 10% in the prior years - mainly owing to tight monetary conditions and lack of access to foreign financing. (2) Central government debt also increased significantly from 81.9% in 2019 to 114.2% in 2022, leading to higher interest expenditure as the government had to pay more interest on the excessive debt obtained. It is also important to note that this interest figure would have been much higher if the accrued interest expenditure on defaulted foreign debt had been included.

Data

Reports

Acts and Gazettes

Insights

Dashboards

Annual Budget Dashboard

Budget Promises

Fiscal Indicators

Fuel Price Tracker

IMF Tracker

Infrastructure Watch

PF Wire

About Us

EN

English

සිංහල

தமிழ்

;

Thank You

Free and Open Access to

Public Finance Data and Analysis

Home

Insights

All

Agriculture and Irrigation

Articles

Budget 2021

Budget 2022

Budget 2023

Budget 2024

Civil Administration

Debt

Defence and Public Order

Education

Employee Provident Fund (EPF)

Energy and Water Supply

Environment

Expenditure

Financing

Health

International Monetary Fund

Revenue

Social Protection and Welfare

Transport and Communication

Urban Development and Housing

Tags

Debt

All

Action Plan

Actual

Annual Report

Appropriation Bill

Asset Management

Audit

Bank

Bonds

Budget

Central Bank of Sri Lanka

Compensation

COPF

Corporate

Covid

Customs Duty

Customs

Debt Management

Debt

Deficit Financing

Development

Disaster

Elections

Employee Provident Fund

Employment

EPF

ESC

Estimate

Excise

Expenditure

External Debt

Finance Act

Financing

Fiscal Policy

Gaming Tax

Gazette

Grant

Health

IMF

Income Tax

Loans

Macroeconomics

Ministry of Finance

Motor Vehicles

National Evaluation Policy

NBT

PAL

Parliament

Performance Report

Procurement

Progress Report

Project Progress

Provincial Council Budget

Public Finance

Remuneration

Reserves

Revenue

Scams

SCL

SOEs

Stamp Duty

State-Owned Enterprises

Tax Exemptions

Tax Incentives

Tax Reforms

Tax Revenue

Tax

Telecommunication Levy

Tobacco

VAT

Data

Reports

Acts and Gazettes

Insights

Filter by year

From

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

To

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

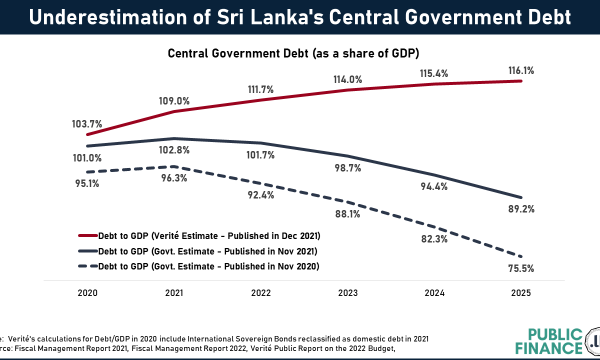

Underestimation of Sri Lanka’s Central Government Debt

Since 2020, the government has revised up its Debt/GDP ratio estimates for the next few years. However, Verité predicts that despite the government’s expectations to decrease debt to GDP to 89.2% by 2...

2021-12-09

View Insight*